Hard Money Loans vs. Soft Money Loans Overview

There is a common misconception that hard money and soft money are defined by their liquidity, with hard money being cash on hand and soft money being paper assets. In reality, these terms refer to the purpose of the loan. Hard money loans are typically used for short-term financings, such as Bridge financing, which is used to fill the gap between the purchase of a new property and the sale of an existing one. Soft money loans, on the other hand, are usually used for long-term investment purposes, such as funding a real estate development project. While hard money loans tend to have higher interest rates, they can be easier to obtain than soft money loans. As a result, it is important to choose the right type of loan for your specific needs.

Start investing

with LBC Capital Income Fund

Hard Money loans overview

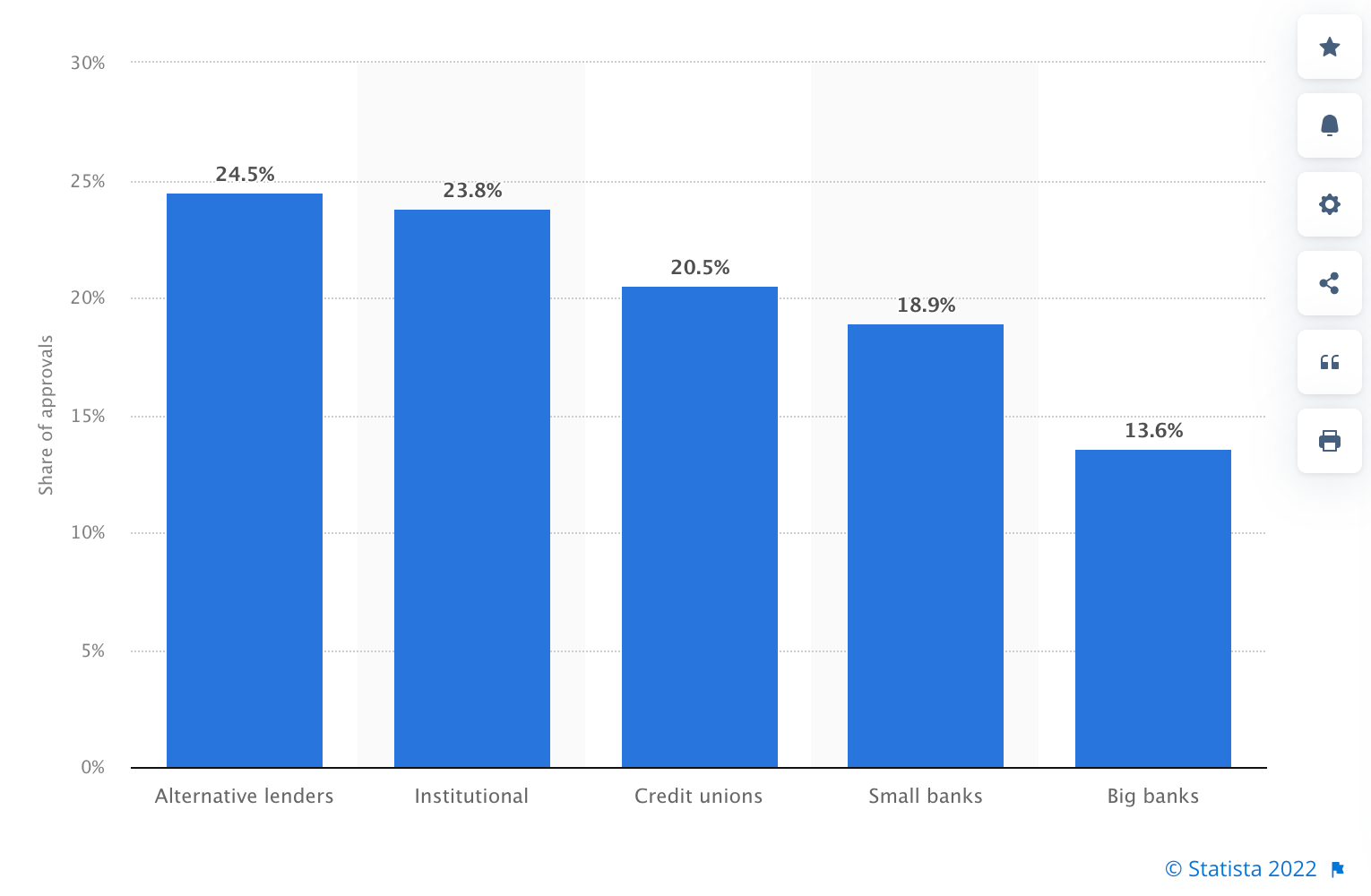

Some time ago hard money meant borrowing cash from a guy with a briefcase full of hundreds and a penchant for breaking kneecaps. Nowadays, it refers to a short-term loan used by real estate investors. While the interest rates on hard money loans are still pretty high, they’re nothing compared to the stomach-churning rates charged by the old-school loan sharks. According to Statista, in 2021 the biggest part of small businesses in the U.S. They approved almost one-fourth of the loan applications received. Such lenders offer hard money loans with a number of advantages, including faster approval times and more flexible terms. As a result, they are well-positioned to meet the needs of small businesses during tough times.

image source: Statista

Hard money loans are made with the intention of being paid back quickly, usually within 12 months. Such loans are different from traditional loans in that they are not based on the borrower’s credit history or income.

Instead, hard money lenders focus on the value of the asset being purchased with the loan.

For this reason, hard money loans tend to be more expensive than traditional loans. However, they can be a good option for borrowers who cannot qualify for a traditional loan or who need to access funding quickly.

The loan amount is determined by the loan to value ratio (LTV), which is calculated by dividing the loan amount by the value of the property. Many hard money lenders will only lend up to 65% of the current value of the property.

Hard money loan benefits

1. Fast closing

Considering the amount of paperwork involved in applying for a bank loan, it’s no wonder that so many people are turning to hard money lenders. Not only is the application process simpler, but hard money loans can often be approved in as little as 24 hours. And with a ten-day closing period, you can get the money you need in a fraction of the time it would take to get a bank loan. So if you’re in a pinch and need some quick cash, a hard money loan may be just what you need.

2. All-in-one financing solution

Some investors choose to use hard money loans because they can be a quick way to gain capital, and the loans can be paid off relatively quickly. Hard money loans are an ideal solution because they can help investors quickly purchase and repair properties so that they can then turn around and sell them for a profit.

3. Flexible terms

Hard money loans can offer more flexible terms than traditional loans, such as interest-only payments or longer repayment periods.

Hard money loans minuses

1. Higher interest rates

Hard money loans are considered to be riskier than traditional loans. For that reason, its rates are also higher.

2. Property equity required

The property equity is used as collateral, so if you’re considering a hard money loan for a purchase price that’s close to the appraised value of the property, it may not be an option. So, it’s important to be realistic about whether a particular property will qualify before applying for a loan.

Soft Money loans overview

The term “soft money” might be new to some, but it’s been around long enough to gain a reputation in the lending industry. Soft money loans are a type of private money lending that offer borrowers the best of both worlds: the security of a traditional loan with the benefits of a hard money loan.

A soft money loan is based on the borrower’s credit score, investing history, and liquid assets instead of the property. That means it’s a great option for investors who need a lot of cash and significant financing in the long term.

While soft money loans require more underwriting than their hard money counterparts, they also come with less risk. That’s because soft money loans are backed by collateral, such as real estate or other property, that can be used to repay the loan if the borrower defaults. Plus, because soft money lenders are typically more lenient when it comes to credit requirements, borrowers who might not qualify for a traditional loan may still be able to get approved for a soft money loan.

Soft money loans pluses

1. Credit score increase

If you are able to repay a soft money loan on time and in full, it can help to improve your credit score.

2. Lower rates

If you’re looking to borrow a large sum of money with relatively little interest, a soft money loan might be for you. With this type of loan, you can typically borrow more than 70% of the property’s value.

Soft money loans minuses

1. Long time closing

The closing period for soft money loans can be lengthy, taking anywhere from 20 to 30 days.

2. Lots of paperwork

Since soft money loans require the check of the borrower’s financial reports, the amount of paperwork required can also be substantial, making it difficult to obtain approval.

3. A good credit score is required

Certified lending institutions that provide soft loans typically require a credit score of 580 or above in order to even consider the loan. As a result, procuring a soft money loan can be a challenge.

Hard Money vs. Soft Money: Key Differences

| Characteristics | Hard Money loans | Soft Money loans |

| Closing | Fast closing in 24 hours | Up to 20-30 days |

| Loan term | Short term | Long term |

| Loan rates | Higher rates | Lower rates |

| Requirements | Negotiable flexible terms and 20% down payment | Rules and restrictions should be followed |

| Paperwork | Minimum paperwork required | Lots of paperwork |

Sum Up

When it comes to taking out a loan, there are two main options: hard money loans and soft money loans. Which one is right for you largely depends on the purpose of your loan application. If you’re looking to buy a personal property that you’ll use in the long run (as opposed to reselling it), then soft money loans are a wiser option. On the other hand, if you’re looking for a loan that will pay for an immediate financial need of a short-term nature, hard money loans are the way to go. So, which one should you choose? The answer, as they say, is up to you.

If you have any questions, feel free to contact us!

Start investing

with LBC Capital Income Fund

Follow our social media channels to stay updated on the latest news:

Latest posts

Blog page

What Is Debt Yield — and Why Some Lenders Use It Instead of LTV

Loan-to-value ratio is the most widely used metric in real estate lending. But for commercial income-producing properties, LTV has a structural weakness: it depends on an appraised value that is itself downstream of a cap rate assumption — a number that can shift significantly based on the appraiser’s judgment. Debt yield uses only observable, auditable […]

What Happens to Your Investment If a Private Lending Fund Manager Fails

One question sophisticated investors rarely ask publicly before committing capital to a private lending fund: what happens to my investment if the fund manager goes out of business, becomes incapacitated, or acts fraudulently? The question matters more than most investors realize — and the answer reveals important structural facts about how well-designed funds protect investor […]